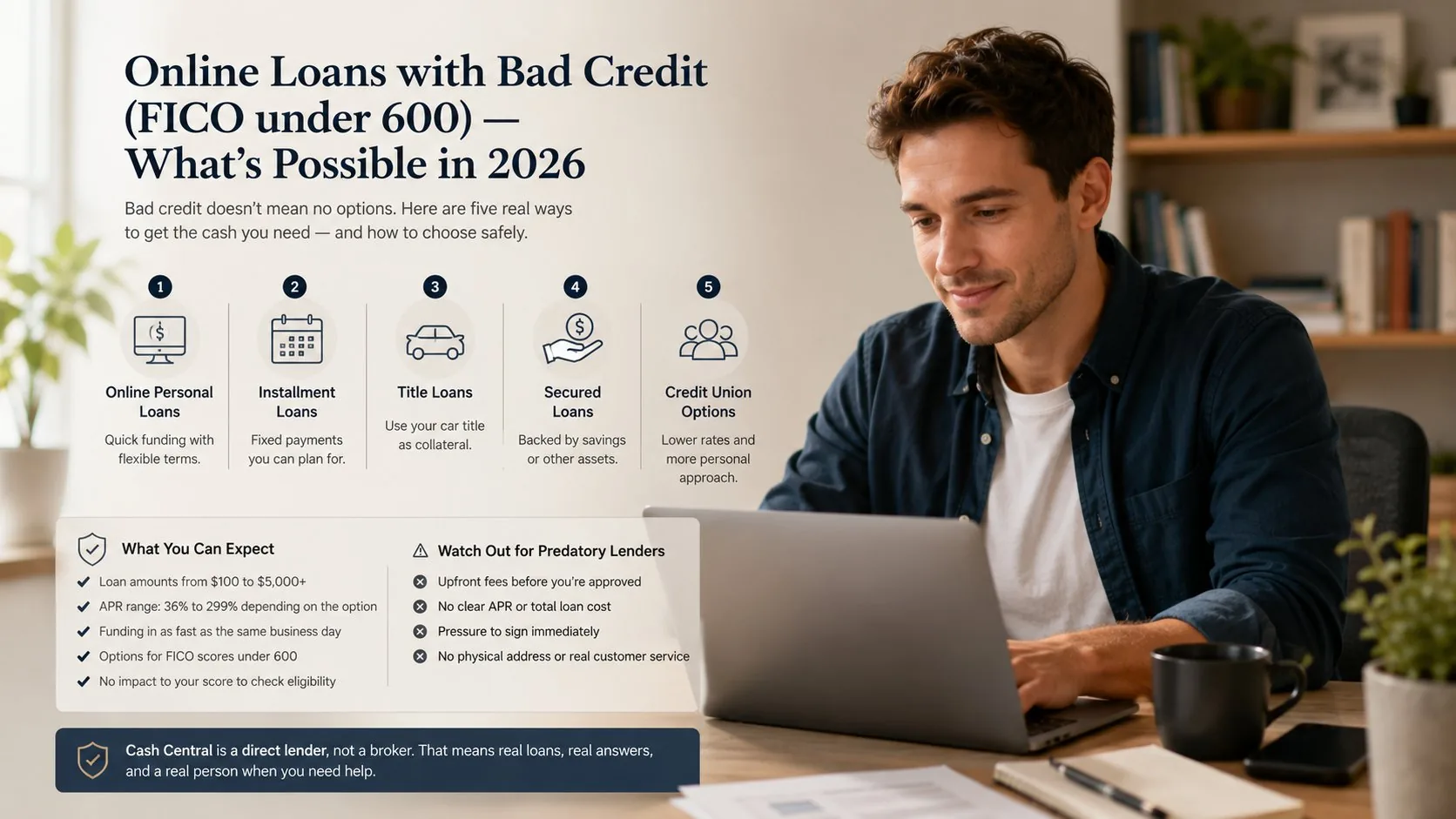

What Is a Payday Loan? A 2026 Beginner's Guide

A payday loan is a short-term, small-dollar cash advance designed to bridge a single expense between paychecks. Understanding how the product actually works — and how its cost is structured — helps you decide whether it's the right tool for the bill you're facing.

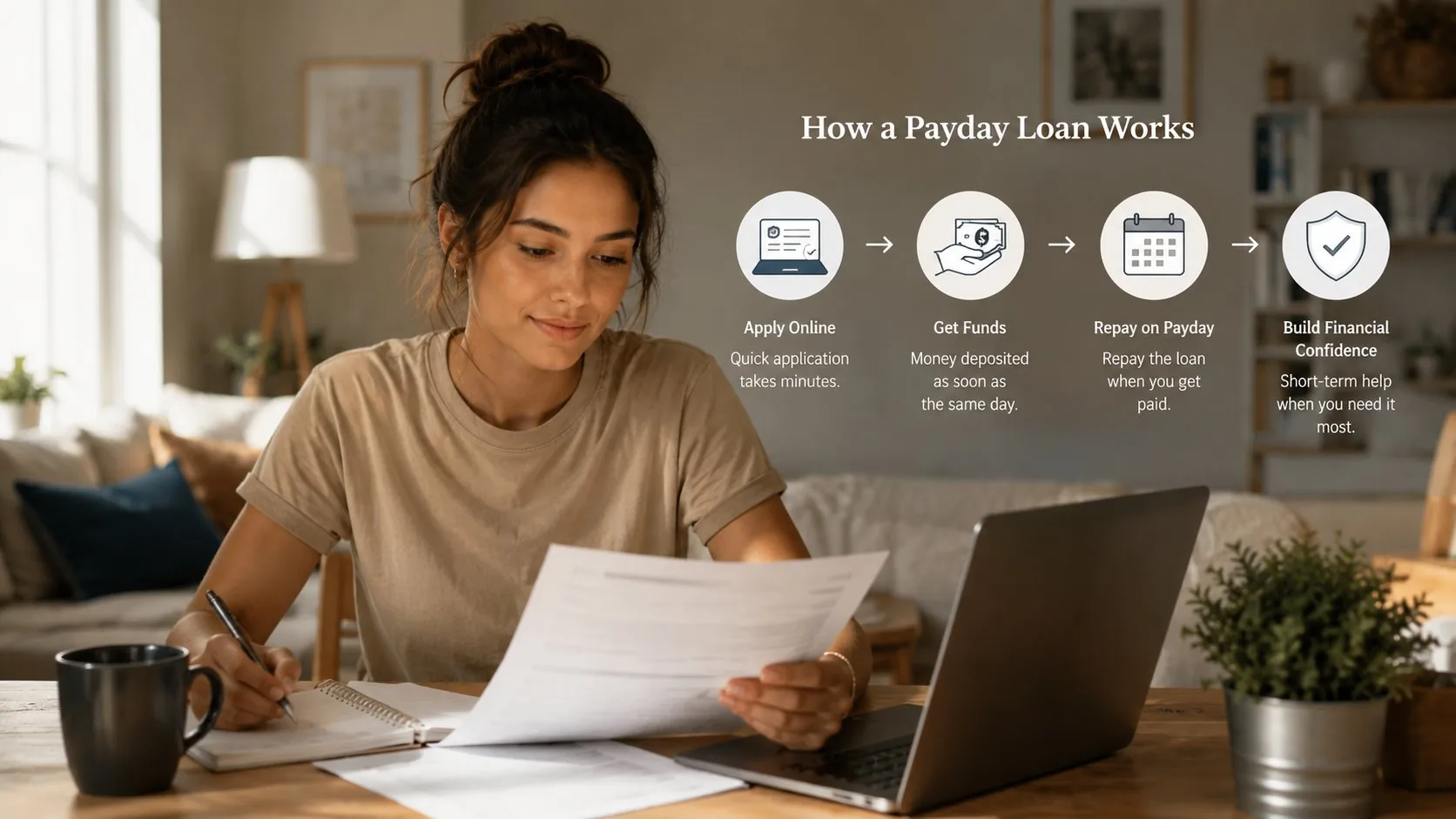

How a payday loan actually works

You borrow a small amount, usually $200 to $1,000, and agree to repay it in full on your next payday — typically 14 to 30 days later. Funds are deposited directly into your checking account, and on the due date the lender debits the same account for the loan plus its fee.

There is no collateral and no multi-month installment schedule. It is one loan, one payment, one short window — built to solve a single, time-sensitive problem.

What you typically need to qualify

Most direct lenders ask for four things:

- You're 18 or older and a U.S. resident

- An active checking account in your name (no pre-paid cards)

- A regular source of income — employment, benefits, or a similar verifiable stream

- A valid government-issued ID

A traditional FICO score is generally not the gating factor. Cash Central, for example, evaluates income consistency and bank-history signals rather than relying on a minimum credit score.

How costs are quoted (and where APR comes in)

Most lenders quote payday-loan costs as a flat fee per $100 borrowed (often $15–$30 per $100, depending on state law). On a 14-day loan that fee structure produces a high annualized percentage rate — sometimes 300%+ — because APR projects what you'd pay if you held the loan for a full year.

For a two-week loan, the more useful number is the total dollar cost: how much will you actually hand back? See our APR explainer for the full math.

When a payday loan makes sense

The honest answer: when the cost of the loan is less than the cost of the alternative. If a single overdraft fee, a missed-shift docked paycheck, or a $45 late penalty would cost more than the loan fee, the loan is the cheaper option.

Classic legitimate uses include medical co-pays, an urgent car repair that lets you keep working, an overdue utility bill where reconnection adds fees, or a one-time gap before a near-certain paycheck.

When it doesn't

Recurring monthly shortfalls. Discretionary purchases. Paying off other debt. These situations don't get solved by short-term credit — they get more expensive. If you're using payday loans repeatedly, that's a signal to talk to a non-profit credit counselor about cash-flow planning.

What's specific to Cash Central

Cash Central is a direct lender, not a broker. Every application, decision, deposit, and payment is handled in-house — no lead-sellers, no third-party processors, no surprise hand-offs. All fees, the total amount due, and the payment date are disclosed before you electronically sign anything.